- Robust economics with after-tax NPV5% of US$498 M, IRR of 43%- and 2.8-year payback under a base case gold price of US$3,100/oz. This further improves to

- US$836 M NPV5% and 62% IRR under a long-term consensus gold price of US$4,000/oz

- US$1,293 M NPV5% and 85% IRR under a spot gold price scenario of US$5,280/oz

- Attractive production profile with average annual production of 92,786 oz Au over the first four years, with all-in-sustaining costs (AISC) averaging US$1,200/oz Au

- Life-of-mine production of 834,858 oz over an ~13 year mine life with AISC averaging US$1,568/oz

- 31.1 Mt ore mined LOM with 3.8:1 strip ratio; average processed grade of 0.89 g/t Au;

- This represents a subset of an updated mineral resource estimate: 1.283 Moz Au indicated resource (58.2 Mt at 0.68 g/t) and 0.09 Moz Au inferred resource (5.6 Mt at 0.52 g/t)

- Approximately 97% of scheduled mill feed is sourced from Indicated material.

Toronto, Ontario--(Newsfile Corp. - March 2, 2026) - Roscan Gold Corporation (TSXV: ROS) (FSE: 2OJ) (OTCQB: RCGCF) ("Roscan" or the "Company") is pleased to announce the results of a positive Preliminary Economic Assessment (the "PEA" or "Study") for the Kandiolé Gold Project in Mali.

"The PEA highlights a robust US$1.29 B NPV5% and 85% IRR under prevailing gold prices, reaffirming our confidence in the Kandiolé project's potential," said Nana Sangmuah, President & CEO of Roscan Gold. "We have a high degree of confidence in this study, which is based on straightforward parameters including a conventional contract-mined open-pit operation feeding a centralized CIL plant, with almost all the ore processed sourced from indicated resources. Importantly, most of the planned mill feed comes from only three of the six deposits included in the resource estimate, highlighting meaningful upside through additional drilling."

"While we see significant potential for further value enhancement, we believe the current scope limits initial capital requirements and represents an opportunity to finance and fast-track the project to production, taking advantage of the robust prevailing gold price and positive capital markets sentiment. This approach should allow us to optimally unlock value from the project and minimize shareholder dilution, while using internal cash flow to pursue opportunities to expand production and extend mine life."

"This PEA marks the first of several key milestones expected this year as we transition toward becoming a developer. Our mining permit application is in the final stages of review, and we anticipate approval in the near term. We have also initiated project financing discussions aimed at securing funding shortly after permits are granted. Environmental baseline work and engineering studies are already underway to support rapid advancement of the project," continued Mr. Sangmuah.

Summary

Bara Consulting (UK) Limited has completed an updated Mineral Resource Estimate (MRE) and Preliminary Economic Assessment (PEA) for the Kandiolé Gold Project in Mali, on behalf of Roscan Resources Corporation. The effective date of the Mineral Resource Estimate is 19 February 2026.

The updated MRE comprises:

- Indicated: 58.2 Mt at 0.68 g/t Au for 1.283 Moz

- Inferred: 5.6 Mt at 0.52 g/t Au for 0.09 Moz

Mineral Resources are reported in accordance with CIM Definition Standards (2014). The updated estimate reflects refined geological domaining and revised estimation parameters, resulting in improved alignment between the interpreted mineralization controls and the reported resource classification.

The PEA evaluates a conventional open-pit mining operation supplying approximately 2.5 Mt per annum (Mtpa) to a centralized carbon-in-leach (CIL) processing facility over an approximately 13-year life of mine (LOM).

The current mine plan incorporates four deposits: Mankouke South, Mankouke Central, Kabaya and KN1.

- Life-of-mine production metrics include:

- Total ore mined: 31.1 Mt

- Total waste mined: 118.1 Mt

- Strip ratio: 3.8: 1

- Recovered gold: 835,693 oz

- Average processed grade: 0.89 g/t Au

Approximately 97% of scheduled mill feed is sourced from Indicated material.

Mineral Resource Estimate

The Mineral Resource Estimate for the Kandiolé Project has an effective date of February 19, 2026 and was prepared in accordance with the CIM Definition Standards (2014).

Mineral Resources are reported above variable break-even cut-off grades derived using reasonable prospects for eventual economic extraction ("RPEEE") assumptions, including a gold price of US$3,000/oz.

The applied cut-off grades are:

- 0.13 g/t Au (Laterite)

- 0.15 g/t Au (Saprolite)

- 0.20 g/t Au (Sap rock and Fresh rock)

The cut-off grades were derived using the following key assumptions:

- Gold price: US$3,000/oz

- Metallurgical recovery: 96% (oxide), 90% (fresh rock)

- Mining cost: US$2.13/t (oxide), US$3.13/t (fresh)

- Processing cost (including tailings): US$8.30-12.25/t depending on material type

- G&A: US$2.50/t

- State royalty: 8%

- Refining and transport: US$3.40/oz

- Payability: 99%

- Mining recovery: 95%

- Mining dilution: 5%

Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability.

The quantity and grade of the Inferred Mineral Resources are uncertain in nature, and there has been insufficient exploration to define these Inferred Mineral Resources as Indicated or Measured Mineral Resources. It is uncertain whether further exploration will result in upgrading them to an Indicated or Measured category.

The Mineral Resource Estimate is subject to risks and uncertainties that could materially affect the estimate, including but not limited to assumptions regarding commodity prices; operating and capital costs; metallurgical recovery; geotechnical and hydrogeological conditions; permitting and regulatory approvals; environmental and social considerations; and the availability of financing. There is no certainty that all or any part of the Mineral Resources will be converted into Mineral Reserves or that the PEA will be realized.

Mining and Processing

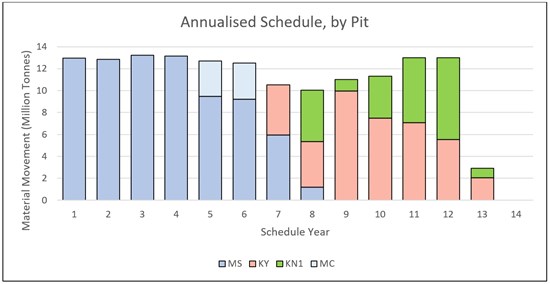

Mining is planned as a conventional open-pit truck-and-shovel operation under a contractor-mining model. Pit optimization and mine design were completed at a gold price of US$2,700/oz. The life-of-mine schedule (Figure 1-1) and cut-off grades applied in the economic model are derived from this optimization case.

Ore will be processed through a conventional crushing, grinding and carbon-in-leach (CIL) circuit incorporating gravity recovery. Metallurgical test work indicates that the mineralization is predominantly free-milling, with overall recoveries ranging from approximately 85% to 97% and an average of approximately 94% under test conditions.

Figure 1. Annualized mining schedule, by pit. (MS=Mankouke South, KY=Kabaya, KN1, Mankouke Central)

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/4821/285931_c844609a34f41ae7_001full.jpg

Infrastructure and ESG Considerations

The Project will require development of supporting infrastructure, including hybrid diesel/solar power generation, site access roads, processing plant facilities, tailings storage facilities, and water supply infrastructure.

A scoping-level Environmental and Social Assessment (ESA) has been completed in accordance with the Malian Mining Code. Baseline studies have characterized environmental and social conditions within the Project area. Further work required to support project advancement includes completion of a detailed Environmental and Social Impact Assessment (ESIA), continued stakeholder engagement, biodiversity management planning, and assessment of potential resettlement requirements.

Closure bonding has been incorporated within sustaining capital estimates.

Cost Estimates

Capital and operating cost estimates have been prepared to a PEA level of accuracy (±30%).

Estimated capital costs (contractor scenario):

- Initial capital: US$218.7 million

- Sustaining capital: US$78.5 million

- Total capital (excluding contingency): US$297.2 million

Operating cost estimates (Table 1) include contract mining, ore haulage, processing, tailings management, and site G&A. Cost assumptions were developed using first-principles modelling and benchmarked against comparable West African gold operations.

Table 1 Unit Operating Costs

| Area | Unit OpEx |

| | Unit | Value |

| Laterite/Saprolite | US$/t rock | 2.45 |

| Sap rock/Fresh | US$/t rock | 3.60 |

| Loading | US$/t rock | 0.50 |

| Haulage to Plant | US$/t/km | 0.15 |

| CIL Processing | US$/t ore | 13.90 |

| Tailings | US$/t ore | 2.00 |

| G&A | US$/t ore | 2.50 |

Economic Analysis

The discounted cash flow (DCF) analysis uses a Base Case gold price of US$3,100/oz and incorporates the Malian fiscal framework, including a sliding-scale State royalty, a 1% NSR royalty, and a 33% corporate income tax.

Under these assumptions, the Project generates:

- After-tax NPV (5%): US$498 million

- IRR: 43%

- Payback: 2.8 years

- AISC Years 1-4: US$1,200/oz

- AISC LOM: US$1,568/oz

The mine schedule, derived from optimization at US$2,700/oz, prioritizes higher-grade material in the initial years, contributing to early cash flow generation and supporting the calculated payback profile.

Sensitivity analysis indicates that project valuation is most responsive to changes in gold price. Variations in capital and operating costs demonstrate comparatively lower proportional impact within the ranges evaluated.

In addition to the Base Case, two higher price sensitivities were evaluated to assess leverage to gold price: a Long-term Consensus case of US$4,000/oz and a Spot Price of US$5,280/oz. The results of the sensitivity are presented in Table 2. Under a US$4,000/oz scenario, NPV increases to US$836M with an IRR of 62%. At a US$5,280/oz spot price scenario, NPV increases to US$1.29B with an IRR of 85%.

Table 2. Kandiolé Project Economics Sensitivity Cases

| Metric | Unit | Price Case |

| Economic Assessment |

| Price Case | US$/Oz | Base Case | Long-Term Consensus | Spot Price |

| Gold Price | US$/Oz | 3,100 | 4,000 | 5,280 |

| Royalty, TC/RC | US$/Oz | 298 | 403 | 510 |

| Asset NPV | US$M | 498 | 836 | 1,293 |

| Payback Period | Years | 2.8 | 2.3 | 2.0 |

| IRR | % | 43% | 62% | 85% |

| Unit Site Cash Costs |

| Mining* | US$/t Ore | 13.40 | 13.40 | 13.40 |

| Haulage to Plant* | US$/t Ore | 1.81 | 1.81 | 1.81 |

| Processing | US$/t Ore | 13.90 | 13.90 | 13.90 |

| G&A | US$/t Ore | 2.50 | 2.50 | 2.50 |

| Total Site Cash Operating Cost | US$/t Ore | 31.62 | 31.62 | 31.62 |

| Cash Cost Summary |

| C1 - Cash Cost | US$/oz | 1,474 | 1,579 | 1,787 |

| M1 Margin | US$/oz | 1,626 | 2,421 | 3,493 |

| AISC | US$/oz | 1,568 | 1,673 | 1,881 |

*The unit mining cost per tonne of ore presented in the economic summary reflects total mining cost (ore and waste) allocated over processed tonnes based on the life-of-mine strip ratio

Conclusions

The Preliminary Economic Assessment indicates that the Kandiolé Project has the technical and economic characteristics to support development as a conventional open-pit gold operation. The mine plan, derived from optimization at a gold price of US$2,700/oz, generates positive economic returns under a Base Case gold price assumption of US$3,100/oz, with an NPV (5%) of US$498 million, an IRR of 43%, and payback within 2.8 years.

Capital intensity and operating costs are consistent with comparable open-pit gold operations in West Africa at a similar scale.

The study is at the PEA level and includes the use of Inferred Mineral Resources, which are considered too speculative geologically to be classified as Mineral Reserves. There is no certainty that the results of the PEA will be realized. Advancement to Pre-Feasibility Study will be required to refine capital and operating cost estimates, reduce technical uncertainty, and further assess environmental and social considerations.

Subject to completion of additional technical studies and permitting processes, the Project presents a coherent development pathway within the current resource envelope.

Technical Information

The PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be classified as Mineral Reserves, and there is no certainty that the results of the PEA will be realized.

The scientific and technical information contained in this news release has been reviewed and approved by Mr. Mark Kenwright, FAusIMM CP(Geo) of African Geos Ltd, who is a Qualified Person as defined by National Instrument 43-101 - Standards of Disclosure for Mineral Projects. Mr. Kenwright has reviewed the information in this news release that relates to the Mineral Resource Estimate and the results of the Preliminary Economic Assessment.

Bara Consulting (UK) Limited prepared the PEA in accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects. The effective date of the Mineral Resource Estimate is February 19, 2026, and the effective date of the PEA is February 27, 2026.

A Technical Report supporting the PEA will be filed on SEDAR+ within 45 days of this news release.

About Roscan

Roscan Gold Corporation is a Canadian gold exploration company focused on the exploration and acquisition of gold properties in West Africa. The Company has assembled a significant land position of 100%-owned permits in an area hosting producing gold mines, including B2Gold's Fekola Mine, which lies on a contiguous property to the west of Kandiolé, as well as major gold deposits located both north and south of its Kandiolé Project in West Mali.

Forward Looking Statements

Certain statements in this news release, including statements regarding the results of the PEA, constitute forward-looking statements within the meaning of applicable securities legislation. Such forward-looking statements are based on the opinions and estimates of management and are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. Forward-looking statements are often, but not always, identified by the use of words such as "seek", "anticipate", "budget", "plan", "continue", "estimate", "expect", "forecast", "may", "will", "project", "predict", "potential", "targeting", "intend", "could", "might", "should", "believe" and similar words suggesting future outcomes or statements regarding an outlook. Such risks and uncertainties include, but are not limited to, risks associated with the mining industry (including operational risks in exploration development and production; delays or changes in plans with respect to exploration or development projects or capital expenditures; the uncertainties involved in the discovery and delineation of mineral deposits, resources or reserves; the uncertainty of resource and reserve estimates and the ability to economically exploit resources and reserves; the uncertainty of estimates and projections in relation to production, costs and expenses; the uncertainty surrounding the ability of the Company to obtain all permits, consents or authorizations required for its operations and activities; and health and safety and environmental risks), the risk of commodity price and foreign exchange rate fluctuations, the ability of the Company to fund the capital and operating expenses necessary to achieve the business objectives of the Company, the uncertainty associated with commercial negotiations and negotiating with foreign governments and risks associated with international business activities, as well as those risks described in public disclosure documents filed by the Company. Due to the risks, uncertainties and assumptions inherent in forward-looking statements, prospective investors in securities of the Company should not place undue reliance on these forward-looking statements.

Readers are cautioned that the foregoing lists of risks, uncertainties and other factors are not exhaustive. The forward-looking statements contained in this press release are made as of the date hereof and the Company undertakes no obligation to update publicly or revise any forward-looking statements contained in this press release or in any other documents filed with Canadian securities regulatory authorities, whether as a result of new information, future events or otherwise, except in accordance with applicable securities laws. The forward-looking statements contained in this press release are expressly qualified by this cautionary statement.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/285931

© 2026 Canjex Publishing Ltd. All rights reserved.